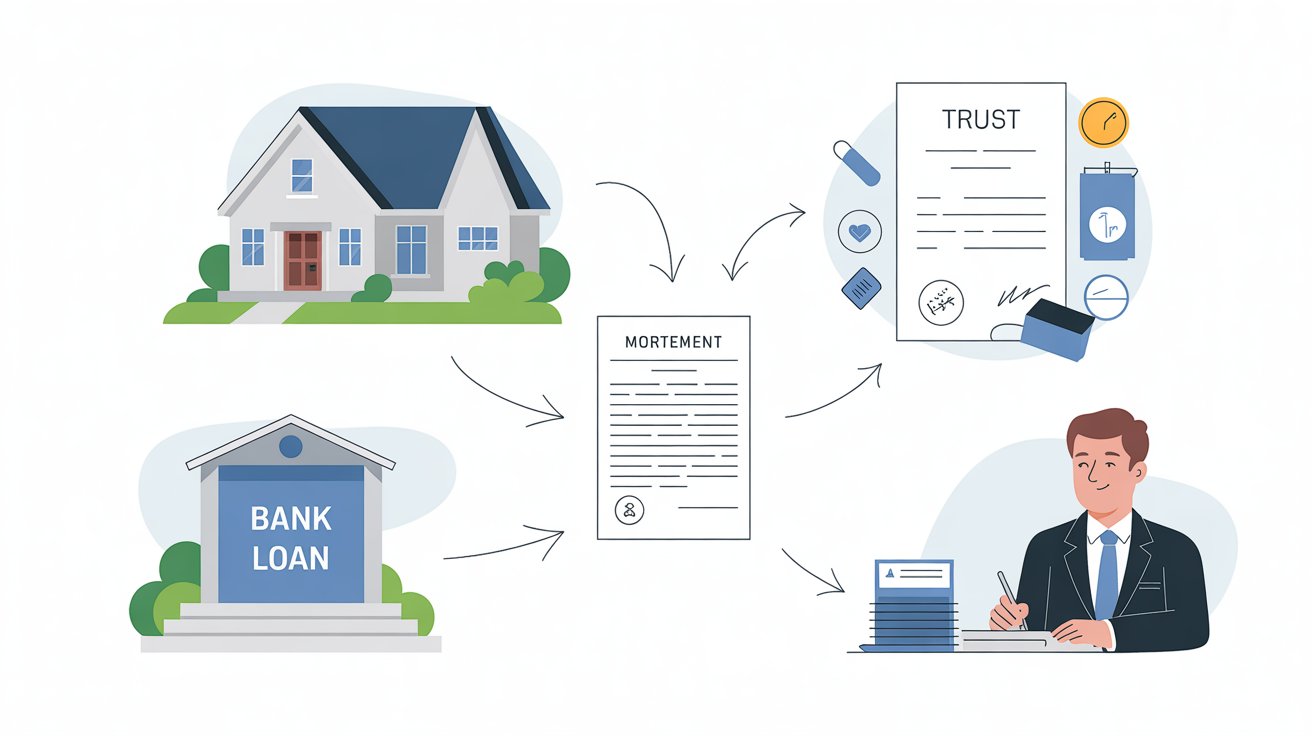

Can a trust take out a mortgage? Yes, it can. But the process is not the same as getting a regular home loan.

I’ve seen a lot of people get confused about this. They set up a trust for estate planning, then run into problems when it’s time to buy or refinance a property. This guide is here to clear that up.

A trust is a legal arrangement where one party holds assets for the benefit of another. Trusts can own real estate. And in many cases, they can carry a mortgage too.

Here’s what I’ll cover: how mortgages work with trusts, the types of trusts that qualify, what lenders need from you, the pros and cons, and the steps to get it done right.

I have worked through this process many times, and I’ll give you a clear picture of what to expect.

Can a Trust Take Out a Mortgage?

Yes. A trust can take out a mortgage. But the type of trust matters a lot.

Most conventional lenders will work with revocable living trusts. The person who created the trust, called the grantor, is still alive and in control. Lenders treat it almost the same as a personal loan.

Irrevocable trusts are a different story. The grantor gives up control when the trust is set up. That makes lenders nervous, because there’s no single person they can hold personally responsible.

Land trusts can also get mortgages, but the process is more specialized and fewer lenders handle them.

The short answer: yes, a trust can get a mortgage, but the path depends on what kind of trust you have.

How Mortgages Work When a Property Is Owned by a Trust

When a trust owns a property, the mortgage is technically in the trust’s name.

But lenders still want a real person on the hook. In most cases, the trustee signs the loan documents personally. Sometimes the grantor does too.

The loan is secured against the property. If payments stop, the lender can foreclose, just like any other mortgage. The trust structure does not protect you from that.

One thing to watch for: some lenders will ask you to remove the property from the trust before approving the loan. Then you move it back after closing. This is more common with conventional loans than with portfolio lenders.

Types of Trusts That Can Get a Mortgage

Not all trusts are treated the same by lenders, and knowing the difference can save you a lot of back-and-forth.

| Trust Type | Mortgage Difficulty | Typical Lenders |

|---|---|---|

|

Revocable Living Trust |

Easy |

Conventional lenders |

|

Irrevocable Trust |

Difficult |

Portfolio lenders |

|

Land Trust |

Moderate |

Specialized lenders |

Revocable Living Trust

This is the most lender-friendly option. You control the trust. You can change it. You can end it at any time.

Fannie Mae and Freddie Mac, the two government-sponsored entities that back most conventional loans in the US, both have guidelines that allow mortgages on properties held in revocable living trusts. The trustee must be the borrower or a named beneficiary. Most major banks are set up to handle this.

Irrevocable Trust

Getting a mortgage with an irrevocable trust is harder. Once assets go in, they stay in. That limits the lender’s options if something goes wrong.

Some portfolio lenders and private lenders will work with irrevocable trusts, but the rates are often higher. You’ll need strong documentation and a clear case.

Land Trust

A land trust keeps the property owner’s identity off public records. It’s common in states like Illinois and Florida.

Getting a mortgage through a land trust requires a lender who knows this type of financing. The beneficial interest in the trust is used as collateral instead of the property title itself.

Requirements to Get a Mortgage in a Trust

Lenders don’t just look at the trust paperwork. They look at the person behind it.

Here’s what they typically need:

- The trust must be valid and properly formed under state law.

- The trustee must have legal authority to borrow against the property.

- Your personal credit score and income still matter.

- The property must be the asset being financed.

- A certification of trust or trust abstract is usually required.

You’ll likely need to provide a copy of the trust agreement. Some lenders also want a letter from an attorney confirming the trust is valid and active.

Pros of Getting a Mortgage Through a Trust

There are real benefits to financing property this way.

Estate planning becomes smoother. When you pass away, the property skips probate and goes straight to your heirs. That saves time and legal fees.

It also adds privacy. The trust name shows up on public records instead of your personal name.

It separates the property from your personal estate, which can help with asset protection in some situations.

And if you own multiple properties, a trust keeps ownership clean and clearly documented.

Cons and Challenges

Not everything about this setup is simple.

Some lenders flat-out won’t do it. Even if the law allows it, not every bank has a process in place for trust mortgages.

The paperwork is heavier. Expect extra documents, a possible legal review by the lender, and a longer timeline to close.

Rates can be slightly higher. Some lenders charge more for trust loans because they view them as more complex.

And if your trust is irrevocable, your financing options shrink significantly.

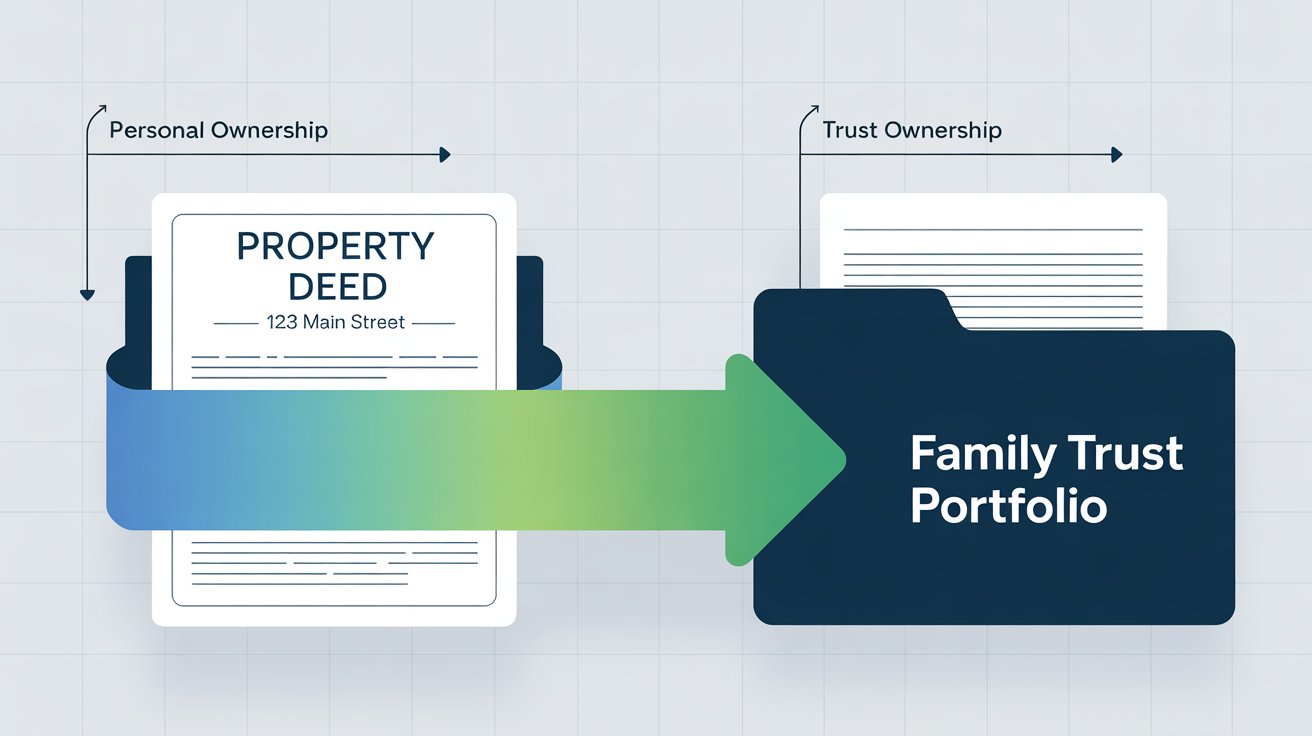

Can You Transfer an Existing Mortgage Into a Trust?

You can transfer the property into a trust after you already have a loan on it. But the mortgage stays in your name. It does not move with the property.

You stay personally responsible for the debt.

One risk worth knowing: some mortgages include a due-on-sale clause. If the lender sees the property was transferred, they can demand full repayment.

Most lenders won’t enforce this for revocable living trusts. That’s because the Garn-St. Germain Depository Institutions Act of 1982 specifically allows homeowners to transfer property into a revocable living trust without triggering a due-on-sale clause, as long as the borrower remains a beneficiary and continues to occupy the home.

It’s still smart to check your loan documents and talk to an attorney before making any changes.

Steps to Get a Mortgage for a Property in a Trust

Follow these steps in order, and you’ll avoid most of the common problems people run into.

- Check if the trust allows borrowing. Read the trust document and confirm the trustee has authority to take on debt.

- Find a trust-friendly lender. Ask upfront before starting an application. Not all lenders handle this.

- Gather your trust documents. You’ll need the trust agreement, a certification of trust, and possibly a letter from your attorney.

- Apply as the trustee. You sign the application in your trustee role, not as a private individual.

- Expect a longer timeline. Trust mortgages often take a few extra weeks compared to standard loans.

- Work with a real estate attorney. This step is worth every dollar. A good attorney catches problems before they get expensive.

Common Mistakes to Avoid

Many people assume any lender will say yes. That’s not true. Call and ask before you apply.

Some people skip reading the trust document first. If the trust doesn’t give the trustee authority to borrow, the whole thing stops right there.

Another common mistake is not telling the lender upfront that a trust is involved. Bring it up on the first call. It saves everyone time and avoids a messy surprise later.

When It Makes Sense to Use a Trust for Real Estate Financing

This setup works best when estate planning is a priority. If you want property to go to your family without going through probate, a revocable living trust is a solid move.

It also makes sense when you own multiple properties and want a clear, organized ownership structure.

If you’re buying an investment property and privacy matters to you, a land trust can work well in states that support it.

But if you’re buying a home with no complex planning needs, keeping things in your personal name is simpler and much easier to finance.

Conclusion

So, can a trust take out a mortgage? The answer is yes in many situations, especially with revocable living trusts.

I’ve covered the key pieces here so you can make a clear decision. Irrevocable trusts take more work. Land trusts need a specialized lender.

The most important step is talking to a trust-friendly lender early in the process. Don’t assume every bank can handle it.

Always bring in a real estate attorney who knows trust law in your state. Getting a mortgage through a trust takes more time and paperwork, but for the right situation, it is worth it. It can make things much smoother for your family down the road.

So here’s my question for you: do you already have a trust in place, or are you just starting to think about this?

Frequently Asked Questions

Can a trust take out a mortgage on a primary residence?

Yes. A revocable living trust can hold a primary residence and still qualify for a conventional mortgage. Fannie Mae and Freddie Mac both allow this, as long as the borrower is the trustee or a beneficiary of the trust.

Does my credit score still matter if the property is in a trust?

Yes, it does. Lenders still evaluate your personal credit, income, and financial history. The trust structure does not replace you as the responsible borrower in the lender’s eyes.

Will transferring my property to a trust trigger the due-on-sale clause?

Usually not for revocable living trusts. The Garn-St. Germain Depository Institutions Act of 1982 protects these transfers under federal law. That said, it’s always smart to review your loan documents and talk to an attorney before making any title changes.

Can an irrevocable trust get a mortgage?

It’s possible, but harder. Most conventional lenders won’t work with irrevocable trusts. You’ll likely need a portfolio lender or private lender, and you should plan for stricter terms and possibly higher rates.

How long does it take to close a mortgage in a trust?

It typically takes a few extra weeks compared to a standard mortgage. The added time goes toward reviewing trust documents, completing a legal review, and clearing extra steps in the underwriting process.