So you’re wondering: can you get a reverse mortgage on a mobile home? You’re not alone.

Many older homeowners in mobile and manufactured homes ask this exact question when retirement funds feel stretched thin.

The short answer is yes, but only if your home meets specific requirements. I’ve researched HUD guidelines and reverse mortgage lending standards to break this down clearly for you.

In this blog, I’ll cover what a reverse mortgage is, how it works, the key requirements you’ll need to meet, payout options, and what to do if your home does not qualify.

I’ll also share smart alternatives worth considering.

Let’s get started.

Can You Get a Reverse Mortgage on a Mobile Home?

Yes, you can get a reverse mortgage on a mobile home, but not on just any mobile home. The home must be a HUD-compliant manufactured home built after June 15, 1976.

It needs to sit on a permanent foundation, and you must own the land it sits on. Most standard mobile homes, especially older ones, will not qualify.

Here’s a quick look at what lenders check:

| Requirement | Needed for Reverse Mortgage |

|---|---|

|

Built after June 15, 1976 |

Yes |

|

Permanent foundation |

Yes |

|

Land ownership |

Yes |

|

Age 62 or older |

Yes |

|

HUD certification labels |

Yes |

|

Primary residence |

Yes |

What Is a Reverse Mortgage?

A reverse mortgage lets homeowners aged 62 and older borrow money against the value of their home.

Instead of you paying the lender each month, the lender pays you. You keep the title to your home.

The loan gets repaid when you sell the home, move out permanently, or pass away. It’s often used as a retirement income tool for people who are house-rich but cash-poor.

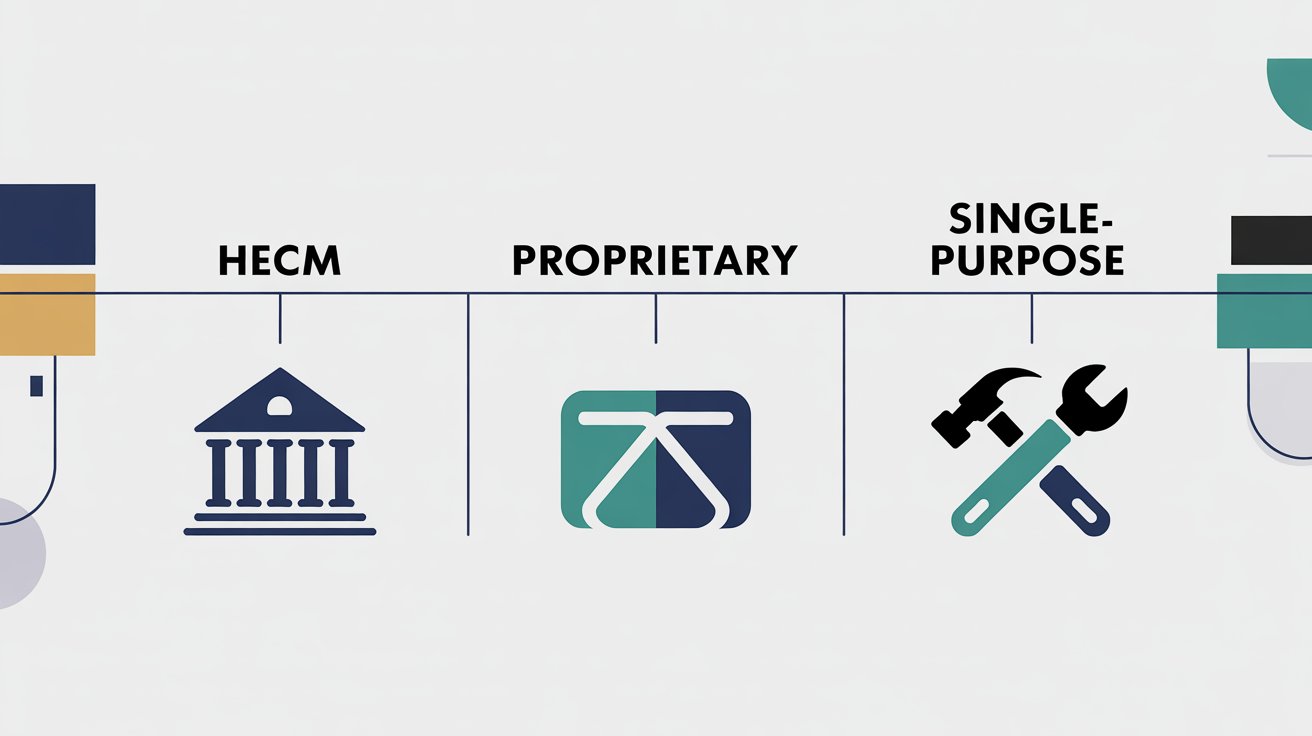

Types of Reverse Mortgages Available

Not all reverse mortgages work the same way, so knowing your options helps you choose the right fit.

Home Equity Conversion Mortgage (HECM)

This is the most common type. It’s backed by the federal government through HUD. For manufactured homes, this is the main option. HECM loans come with rules and protections built in for the borrower.

Proprietary Reverse Mortgages

These are private loans offered by lenders. They are not government-backed. Most lenders offering proprietary reverse mortgages won’t cover mobile or manufactured homes.

Single-Purpose Reverse Mortgages

These are offered by state and local agencies. They’re meant for one specific use, like home repairs or property taxes. They’re less common but can help in certain situations.

Mobile Home vs Manufactured Home: Why the Difference Matters

The terms sound the same. They’re not.

A mobile home typically refers to a factory-built home made before June 15, 1976. These were built under older, looser standards.

A manufactured home was built after that date under strict HUD standards. This distinction is critical because lenders only consider manufactured homes for reverse mortgages.

If your home was built before 1976, it likely will not qualify.

Requirements to Get a Reverse Mortgage on a Mobile Home

Your home has to clear a specific checklist before any lender will move forward with you.

According to guidelines from the U.S. Department of Housing and Urban Development (HUD), manufactured homes must meet federal construction and safety standards to qualify for a HECM reverse mortgage.

Age Requirement: You must be at least 62 years old. If there are co-borrowers, all of them must meet this age requirement.

HUD-Compliant Manufactured Home: The home must be built after June 15, 1976. It must meet HUD’s manufactured home construction and safety standards.

Permanent Foundation Requirement: The home must be attached to a permanent foundation. It cannot be on wheels or a temporary setup. A licensed engineer may need to confirm this in writing.

Property Must Be Your Primary Residence: You must live in the home full-time. Vacation or rental properties do not qualify.

You Must Own the Land: You must own the land the home sits on. If you rent the lot, most lenders will not approve the loan.

HUD Certification Labels and Data Plates: The home must have HUD certification labels on the outside. It also needs a data plate inside, usually found in a cabinet or bedroom. These confirm the home was built to HUD standards.

When a Mobile Home Does NOT Qualify

Your mobile home won’t qualify if it was built before June 15, 1976. It also won’t qualify if it’s in a mobile home park where you rent the land.

Homes without a permanent foundation are also disqualified. Missing HUD labels or data plates can be a problem too.

In these cases, you’ll need to look at other options.

How Much Money Can You Get From a Reverse Mortgage on a Mobile Home?

The amount depends on a few factors. These include your age, the home’s appraised value, current interest rates, and how much equity you have.

Manufactured homes often appraise lower than site-built homes. So the loan amount may be smaller.

A HUD-approved counselor can give you a clearer estimate before you apply.

Reverse Mortgage Payout Options

Once approved, you get to choose how you receive the money. There are three main ways lenders pay you.

Lump sum means you get the full amount in one payment upfront. This works well if you have a large expense to cover right away, like medical bills or home repairs.

Monthly payments give you a set amount every month. This works like a steady income stream and helps cover regular living costs over time.

A line of credit lets you draw money only when you need it. The unused portion can grow over time, making this a flexible option for many borrowers.

Some lenders also offer a mix of these. Talk to your lender about what fits your situation best.

Pros of Getting a Reverse Mortgage on a Mobile Home

There are real benefits here, especially if retirement income is tight and you plan to stay in your home long-term.

- No monthly mortgage payments required

- You can stay in your home while receiving funds

- Multiple payout options available, including lump sum, monthly payments, and line of credit

- Can supplement retirement income without selling your home right away

- Loan proceeds are generally not considered taxable income

Cons and Risks to Consider

That said, this loan comes with trade-offs that are worth understanding before you commit to anything.

- Loan balance grows over time as interest and fees add up

- Your heirs will inherit less equity after you’re gone

- Missing property tax or insurance payments can trigger early repayment

- Manufactured homes often appraise lower, reducing how much you can borrow

- Closing costs and fees can be significant

Alternatives if Your Mobile Home Doesn’t Qualify

If a reverse mortgage is off the table, you still have solid options worth looking into.

Home Equity Loans

If you have equity and decent credit, a home equity loan may work. These are harder to get on manufactured homes but not impossible with the right lender.

Cash-Out Refinancing

You refinance your current mortgage and take out extra cash. This requires qualifying based on income and credit score.

Selling the Mobile Home

Selling can give you a lump sum to fund retirement. You could downsize to a cheaper property or rent instead.

Property Tax Relief Programs

Many states offer tax relief programs for seniors. These can reduce your monthly costs without taking on new debt.

Downsizing

Moving to a smaller, less expensive home can free up cash. It’s practical and can make a real difference in your monthly budget.

Step-by-Step: How to Apply for a Reverse Mortgage on a Mobile Home

The process is straightforward once you know what to expect at each stage.

Step 1: Check if your home qualifies. Look at the build date, foundation type, and land ownership status.

Step 2: Find your HUD certification labels and data plate.

Step 3: Talk to a HUD-approved counselor. This is required by law before you apply.

Step 4: Choose a lender that offers HECM loans for manufactured homes.

Step 5: Get a home appraisal from a licensed appraiser.

Step 6: Submit your application and go through the underwriting process.

Step 7: Close on the loan and receive your funds in your chosen payment format.

Costs and Fees to Expect

Reverse mortgages are not free.

You’ll typically pay an origination fee, mortgage insurance premiums for HECM loans, closing costs, and ongoing servicing fees. These can total several thousand dollars.

They’re often rolled into the loan balance, so you don’t pay out of pocket upfront. But they do reduce how much equity you keep over time.

Conclusion

So, can you get a reverse mortgage on a mobile home? Yes, but only if the home meets HUD manufactured housing standards and other lender requirements.

Your home has to sit on a permanent foundation, and you need to own the land. Many older mobile homes simply won’t make the cut.

That’s okay. I’ve shared several alternatives that might work better for your situation. From tax relief programs to selling or downsizing, there are more paths than you might expect.

Take your time with this decision. Talk to a HUD-approved counselor first. It’s a free service and one of the smartest steps you can take before signing anything.

Is your manufactured home meeting the qualifications for a reverse mortgage, or are you leaning toward one of the alternatives shared here?

Frequently Asked Questions

Does a mobile home qualify for a reverse mortgage?

Only manufactured homes built after June 15, 1976 and meeting HUD standards can qualify. Older mobile homes typically do not meet the requirements for a reverse mortgage.

Can you get a reverse mortgage on a mobile home if it’s in a park?

Most lenders require you to own the land your manufactured home sits on. If you’re renting the lot in a mobile home park, you will generally not qualify for a reverse mortgage.

What year must a mobile home be for a reverse mortgage?

Manufactured homes must be built after June 15, 1976, when HUD construction standards took effect. Homes built before that date do not meet the federal requirements for a HECM reverse mortgage.

What happens to my reverse mortgage when I pass away?

Your heirs will need to repay the loan. They can do this by selling the home or refinancing it into a traditional mortgage within a set time frame.

Is a HUD counseling session required before applying?

Yes. Federal law requires you to complete a counseling session with a HUD-approved agency before a HECM reverse mortgage can be issued to you.