After researching IRS guidance, estate tax rules, and real estate sales across multiple cases, I’ve found the step-up basis rule is the biggest factor affecting inherited property taxes.

This guide breaks down exactly how is inherited property taxed when sold, from capital gains and deductions to special situations and common mistakes.

I’ll also show you ways to reduce what you owe before you close the sale. No legal jargon here, just the facts you need to move forward.

Many people ask how inherited property is taxed when sold, especially when they inherit a home or rental property.

I want to make this clear and useful for you from start to finish.

The Short Answer: How Is Inherited Property Taxed When Sold?

When you sell inherited property, you typically owe capital gains tax on the profit.

The good news?

The IRS usually measures your profit from the date of the original owner’s death, not the price they paid years ago.

This is called the step-up in basis. It often means you owe little to no tax, especially if you sell soon after inheriting.

Understanding the Step-Up in Basis Rule

Understanding the capital gains tax on inherited property starts with the step-up in basis rule, and it’s the most important concept in this entire guide.

What “Step-Up in Basis” Means

Your basis is what the IRS considers your starting cost in the property. Normally, that’s the original purchase price.

With inherited property, your inherited property tax basis steps up to the fair market value on the date the original owner died.

So if they bought a home for $100,000 and it was worth $400,000 when they passed, your basis becomes $400,000. That’s a huge difference.

How the IRS Calculates the New Property Value

The IRS uses the fair market value at the date of death. A professional appraisal usually establishes this number.

In some cases, a filed estate tax return (Form 706) will set the value. Keep all appraisal documents. You’ll need them when you sell and report the gain or loss on your taxes.

The appraisal process matters more than most people realize. A certified appraiser will assess the property condition, comparable sales in the area, and local market data at the time of death.

That report becomes your legal basis for the stepped-up basis real estate calculation. Do not skip this step.

When Step-Up Does NOT Apply

The step-up rule does not apply to gifted property. If the original owner gave you the property before they died, you take their original basis, not the stepped-up value.

Gifts and inheritances are treated differently by the IRS. If property was held in an irrevocable trust, different rules may apply there too.

Timeline: What Happens Before You Can Sell Inherited Property

Selling inherited property often involves a few legal steps before the sale can happen.

Many people don’t realize there’s a process to work through first, and skipping any step can delay the sale or create tax complications.

Here’s a typical timeline:

- Property owner passes away

- Estate enters probate, if required

- Property is appraised to establish fair market value

- Ownership transfers to the heirs

- Property is listed for sale

- Sale closes and capital gains are calculated

Probate is the legal process that confirms ownership before anything can be transferred or sold. Depending on the state, this can take a few months to over a year.

If the property was held in a living trust, probate may be avoided entirely and the sale can happen much faster.

One important note: the appraisal in step three is not just a formality. It sets your stepped-up basis, which directly affects how much tax you owe when you sell.

Getting it done properly at the start protects you later.

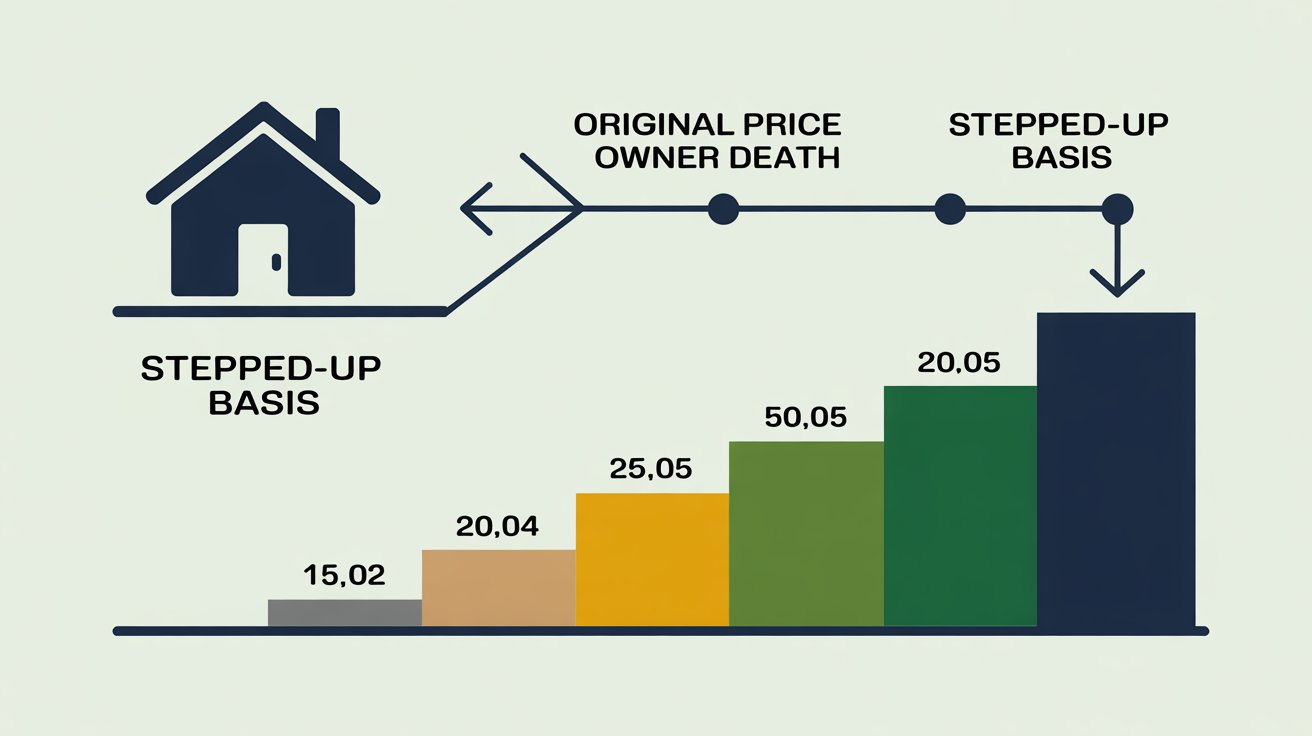

Example: How Taxes Work When You Sell Inherited Property

Say your parents bought a home in 1985 for $80,000.

When they passed in 2024, it was worth $500,000. You inherited the home and sold it eight months later for $510,000.

Your gain is just $10,000, which is $510,000 minus your $500,000 stepped-up basis. You’d owe capital gains tax on that $10,000, not on the full increase from $80,000.

That’s the step-up rule working in your favor.

Here’s a simple breakdown of that same example:

| Sale Price | Step-Up Basis | Taxable Gain |

|---|---|---|

|

$510,000 |

$500,000 |

$10,000 |

|

$530,000 |

$500,000 |

$30,000 |

|

$500,000 |

$500,000 |

$0 |

|

$480,000 |

$500,000 |

($20,000) Loss |

The table above shows how the taxable gain changes based on the final sale price. A lower sale price can even create a deductible loss in some cases.

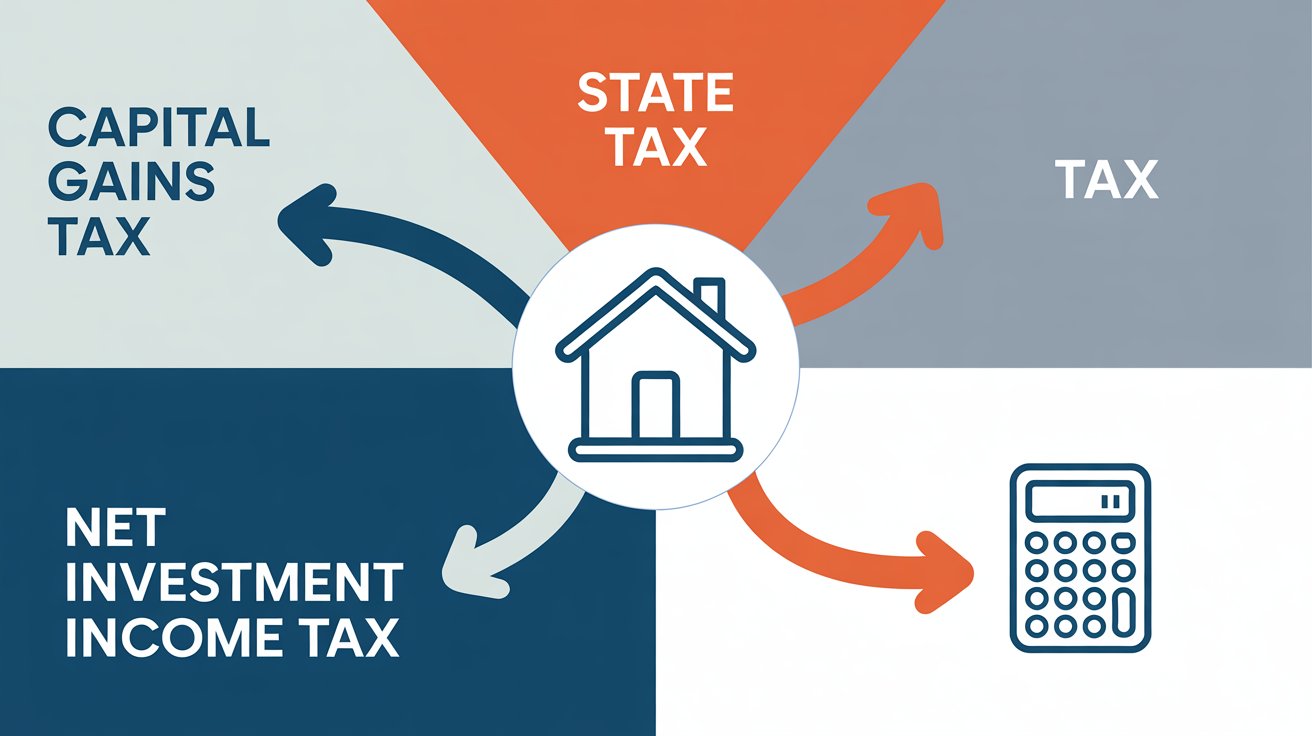

What Taxes You May Owe When Selling Inherited Property

The tax consequences of selling inherited property go beyond just one federal rate. Several taxes can apply depending on your income, your state, and how the property was used.

Capital Gains Tax

Inherited property is treated as a long-term asset by default, regardless of how long you held it. That means you pay long-term capital gains rates, which are lower than ordinary income tax rates. The federal rates are 0%, 15%, or 20%, depending on your total taxable income for the year.

State Capital Gains Taxes

Some states also tax capital gains. States like Texas and Florida have no income tax. California, on the other hand, taxes capital gains as regular income. Check your state’s specific rules, because state taxes can add a significant amount to your total bill.

Net Investment Income Tax (NIIT)

If your total income exceeds $200,000 as a single filer, or $250,000 for married filers, an extra 3.8% NIIT may apply to your capital gain. This is layered on top of your regular capital gains tax. High-income earners need to factor this in when estimating what they’ll owe.

How Much Tax Do You Pay on Inherited Property Sales?

The exact amount depends on your income, your state, and your gain. Here’s how the federal rates break down for most sellers.

Current Long-Term Capital Gains Rates

The federal long-term capital gains rates are 0%, 15%, and 20%, depending on your taxable income. Income thresholds adjust each year for inflation, so confirm the current numbers with a tax professional when you file.

State taxes and NIIT are added on top of these federal rates and can push your effective rate higher than expected.

How to Reduce Taxes When Selling Inherited Property

There are several legal ways to lower your taxes when selling inherited real estate, and knowing them before you sell makes a real difference.

Sell Soon After Inheritance

The step-up basis locks in the value at the date of death. Selling relatively soon after inheritance often keeps the taxable gain minimal because the step-up basis reflects the property’s value at the time of death. That keeps your gain small and your tax bill low.

Deduct Selling Expenses

You can subtract selling costs from your taxable gain. These include real estate commissions, closing fees, and legal costs. These deductions shrink your net profit, which directly reduces the tax you owe.

Account for Improvements

If you made improvements to the property before selling, those costs can increase your basis. A new roof, kitchen renovation, or HVAC replacement all count. Keep receipts. Each dollar you add to the basis is a dollar less of taxable gain.

Use Capital Loss Offsets

If you had other investments that lost money in the same tax year, you can use those losses to offset your capital gain. This strategy is called tax-loss harvesting, and it’s a simple way to reduce your overall tax bill.

Convert Property to Primary Residence

If you move into the inherited home and live there for at least two out of five years, you may qualify for the primary residence exclusion. Single filers can exclude up to $250,000 of gain. Married filers can exclude up to $500,000. That’s a major tax break.

Consider a 1031 Exchange (in some cases)

If the inherited property is an investment or rental, a 1031 exchange may let you roll the sale proceeds into another investment property and defer capital gains taxes. Strict timing rules apply, so get professional advice before going this route.

Special Situations That Change the Tax Rules

Not every inherited property sale follows the same path. These four situations can shift how is inherited property taxed when sold in significant ways.

Inherited Property With Multiple Heirs

When multiple people inherit the same property, each heir reports their portion of the gain on their own tax return. If heirs disagree about selling, a partition agreement or court involvement may be needed. Each person’s share of the gain is taxed separately.

Inherited Rental Property

Rental property still gets the step-up in basis when inherited. But if you continue renting it out and later sell, you may face depreciation recapture. The IRS taxes recaptured depreciation at 25%, which is separate from the capital gains rate. This is one of the more complex inherited property sale taxes to plan around.

Property Held in a Trust

Property from a revocable trust usually qualifies for the step-up in basis. An irrevocable trust may not. The tax treatment depends on how the trust was structured. Always review the trust documents with a tax professional before assuming the step-up applies.

Inherited Property From a Spouse

In community property states like California, Texas, and Arizona, a surviving spouse often gets a full step-up on the entire property. In non-community property states, only the deceased spouse’s half gets stepped up. This distinction can mean a significant difference in the final tax bill.

Do You Pay Estate Tax and Capital Gains Tax?

These are two separate taxes.

Estate tax is paid by the estate before assets are distributed to heirs. Capital gains tax is your responsibility when you sell.

You generally do not pay both on the same profit. Still, large estates may trigger both, so it’s worth confirming with an estate attorney or tax advisor.

IRS Forms You May Need When Selling Inherited Property

When you sell inherited property, you’ll typically need Schedule D and Form 8949 to report the sale on your federal tax return.

If the estate filed Form 706, that document establishes the stepped-up basis. Keep all appraisals, closing statements, and any estate paperwork in one place.

You’ll need them when filing.

Common Mistakes People Make When Selling Inherited Property

These mistakes cost people real money, and most of them are easy to avoid once you know what to look for.

- Using the original purchase price as the basis instead of the stepped-up value at the date of death

- Skipping a professional appraisal and guessing the fair market value

- Not deducting selling costs like commissions, closing fees, and legal expenses

- Ignoring the NIIT, which adds 3.8% for higher-income sellers

- Overlooking state-level capital gains taxes entirely

- Forgetting to account for home improvements that increase your basis

- Waiting too long to consult a tax professional before signing the closing documents

Working with a tax professional before closing the sale can help you avoid all of these and keep more of the proceeds in your pocket.

Key Takeaways About Taxes on Inherited Property Sales

Inherited property gets a step-up in basis to fair market value at the time of death. You pay long-term capital gains tax on any profit above that new basis.

Federal rates are 0%, 15%, or 20% and adjust for inflation each year. State taxes and NIIT may also apply.

Strategies like selling quickly, accounting for improvements, using capital loss offsets, or converting to a primary residence can lower your bill.

Always document the stepped-up basis real estate value and consult a tax professional before you sell.

Conclusion

Figuring out how is inherited property taxed when sold does not have to be stressful. The step-up in basis rule alone can save you a significant amount of money.

I’ve seen many people overpay simply because they didn’t know their inherited property tax basis or assumed the original purchase price still applied.

Once you understand your basis, what taxes apply, and what you can legally deduct, the process gets much clearer. Every situation is a little different.

A rental property is not the same as a family home. Multiple heirs add layers.

Trusts can shift the rules entirely. That’s why getting a tax professional involved before you sign anything is a smart move.

The more informed you are, the better your outcome will be.

Have a question about your specific inherited property situation you haven’t found the answer to yet?

Frequently Asked Questions

Do I have to pay taxes on inherited property right away?

No. You only owe tax when you sell the property, not when you receive it. The tax clock starts at the closing date of the sale, so there’s no immediate bill just for inheriting.

What if the inherited property has gone down in value?

If you sell for less than your stepped-up basis, you may be able to claim a capital loss. That loss can offset other gains or reduce ordinary income by up to $3,000 per year.

Is inherited property considered income?

No. The IRS does not treat the inheritance itself as taxable income. Capital gains tax on inherited property only applies when you sell for more than your stepped-up basis at the time of death.

How long do I have to sell inherited property to avoid taxes?

There’s no set deadline, but selling relatively soon after inheritance often keeps the taxable gain minimal because the step-up basis reflects the property’s value at the time of death.

Do all states have an inheritance tax?

No. As of 2026, only six states have an inheritance tax: Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. This is separate from capital gains tax and depends on your state of residence.